- ПьНнЫбЫї

- ШЋеОЫбЫї

Agile delivery capabilities are of critical importance: this approach is smart by design and is not intended to happen “automatically.” Governance and performance-management tools are also critical, as they are in any transformation: for transformative ways of working to stick, performance has to be managed for the new norm at the outset, across all organizational silos.

Target state

Rapid-process digitization is relevant to nearly half of a bank’s cost base. It works process by process and can lead to lower costs, higher productivity, faster delivery times, and reduced customer leakage. As it proceeds, rapid-process digitization transforms the operating model—processes are consolidated, functionalized, and outsourced or offshored as needed.

Ёё Channels, including branches, call centers, ATMs, and Internet. Channels are optimized to enable efficient downstream processing, including electronic data capture in all branches and programs implemented to encourage migration to digital channels.

Ёё Business (retail, commercial).Business is focused on product strategy, sales, and distribution (for example, branches that are focused only on sales, with all fulfillment done in operations).

Ёё Operations.Operational processes are managed end to end, with more than 600 processes defined and categorized into automated and partly automated; lean management is also applied, with tailored metrics and management models.

Ёё IT. All infrastructure functions are centralized, including operations, IT, finance, risk, human resources, procurement, and fraud; processes are configured into cross-business utilities (for example, payments and complaint management).

Ёё Other infrastructure, including human resources and finance.Offshore locations are leveraged where relevant and work-flow tools dynamically allocate work across the footprint.

This approach creates the desired customer experience and substantially reduces customer-value leakage. In mature markets, we have seen this approach improve productivity by 30 to 90 percent, measured in both cost and time to deliver, in almost half of a bank’s total cost base. In emerging markets, the impact can be even greater. The approach improves overall risk management and management transparency by optimizing and clarifying the underlying methods for each process. It also enables a more fundamental transformation of the operating model, including consolidation, offshoring, or even outsourcing processes.

Rapid-process digitization allows banks to surmount the barriers and complexities of their lagging operating models and meet the challenges of a digital-banking future. The approach delivers dramatic performance improvements quickly: in our experience, great value can be realized in a matter of months or even weeks. The benefits are indeed many, since the approach is comprehensive. Even when an accelerated program is adopted, the choice of focus is based on a complete understanding of the total process landscape.

The levers for achieving the next-generation banking experience are in place, well understood, and more straightforward than many bankers would think. Most important, the next generation of high-value customers will expect their bank to offer a seamless digital experience. If they don’t find it at their bank, they will look for it elsewhere.

Chapter 6 Gearing the IT engine for digital banking

(Andy Holley, Robin Loh, and Parker Shi)

Executive summary:

Ёё For businesses to perform optimally, IT infrastructure and applications must be aligned.

Ёё A recent study of Asian banking’s IT terrain demonstrated a divergence in IT efficiency and value delivery; it also showed emerging-market banks outperformed their developed-market peers.

Ёё Winners positioned IT strategically, ensuring CIOs are present in the boardroom, focusing on effective operating practice, and emphasizing strong vendor management.

Ёё As consumer sophistication grows and expectations shift, it will only become more important to have a robust IT engine.

Ёё Asian banks should embrace five fundamental capabilities, including a business-technology organization and next-generation infrastructure, to remain competitive—or even leapfrog more advanced players.

Ёё Innovative risk management means creating the basis for competitive advantage by leveraging unconventional data or using a methodological approach to leveraging qualitative data.

For banks to deliver on the promises of digital banking without adding needless complexity and cost, their IT operating models must be transformed in line with global best practices. IT infrastructure and applications must be strategically aligned to enhance business performance. The experience ofAsian banks in doing this has not been essentially different from that of their Western counterparts.

A recent McKinsey benchmarking study of IT in Asian banking revealed a landscape that will be very familiar to those acquainted with the IT terrain of global banking. The study disclosed wide divergence in IT efficiency and value delivery, which did not correlate to bank size, and also showed emerging-market banks outperforming their developed-market peers. The winners were thus not necessarily the largest banks or those banks operating in the most advanced geographies. Rather, winners were those banks that positioned IT more strategically, reaching beyond the usual cost-center models, with more CIOs having meaningful boardroom presence. These banks follow better operating practices with stronger business-IT alignment and effective IT complexity management. They also practice stronger vendor management while outsourcing more selectively, emphasizing maintenance in outsourcing rather than development.

Five fundamental capabilities

Banks need powerful IT capabilities to truly enable digital banking. Inefficient and piecemeal approaches will create IT bottlenecks rather than business value. An efficient IT engine for the digital bank rests on five fundamental capabilities:

1. A business-technology organization

2. A continuous solutions process

3. Next-generation infrastructure

4. A simplified technology ecosystem

5. Advanced analytics and data management

In examining each capability in turn, we have tried to balance demands for achieving business objectives with the need to avoid inessential complexity. Especially helpful in understanding this balance has been our experience of working with both digital leaders and leading “digital transformers,” and examples from this experience are included in the following discussions.

Across the uneven Asian banking IT terrain, some banks are deeply engaged in the IT transformation needed to enable digital banking (see sidebar, “Stuck in the moment or on the move?”). Leaders have already emerged, having positioned IT strategically, as an effective business enabler. These Asian leaders have achieved best-in-class operations and business performance, driving improvements with investments in IT innovation for growth and continuous tracking of performance.

1ЃЎA business-technology organization

At the heart of the digital enterprise lies a fundamentally different model of how business and IT work together. In this new business-technology organization, IT becomes a strategic center for business innovation, transforming the way the business is run and constantly cocreating value with business partners.

The business-technology organization goes well beyond governance, reporting lines, and classic demand management, challenging traditional concepts of business and IT alignment. In the new model, business and IT talent are required to work together in such an integrated way that the boundaries between the two begin to blur. The reason this is happening is not far to seek: customer expectations of a rich, always-available online experience are drawing together business and IT threads, toward integration. In order to meet those expectations and deepen their share of wallet, banks must offer holistic digital-banking solutions that keep pace with customer banking needs and technological preferences.

This new form of business-IT integration permeates all parts of the IT operating model, creating, in effect, a true business-technology operating model: plan, design, build, and run. Based on our work with leading digital transformers, we have identified a set of key priorities on the path toward establishing the new business-technology organization, spanning strategy, governance, and organizational alignment; particular attention must be paid as well to winning the “war” for digital talent:

Ёё Build an equal business-IT partnership, in which IT is involved in all business decisions, providing digital insights to execute but also to shape the bank’s overall strategy.

Ёё Rather than a separate IT organization for digital banking, consider creating a high-performing digital lab within the legacy IT organization, which reports directly to the CIO.

Ёё Create closer integration between IT and operations to enable rapid, clean-sheet process digitization.

Ёё Plan on winning the war for digital talent, which will entail several elements:

– Overhaul role and skill definitions to cater to the digital world (for example, designate a “velocity manager”).

– Renew talent-search methods to include crowdsourcing and distributed cocreation.

– Identify the bank’s unique selling points for top IT talent compared with companies such as Apple, Facebook, and Google, including clear career pathways.

2ЃЎA continuous solutions process

A spectrum of solutions approaches can be observed in Asian banks today, with delivery models ranging from “agile” to the traditional sequential “waterfall” model. As digital banking becomes the norm, however, all players will have to move toward models that allow for continuous solutions development. Traditional models like the waterfall are fundamentally challenged by the requirements of digital banking, as they are not suited to withstand competitive pressures to innovate or to meet the ever-rising expectations of the modern digital customer. Digital leaders are therefore adopting continuous solutions processes, which flow naturally from the fundamental strategic premises of the digital enterprise.

An iterative approach

Continuous solutions are defined by an iterative development process, including rapid prototyping of hypothesized models, for creating implementable solutions within four- to eight-week cycles. The cycles are designed to capture frequent user feedback, which improves the responsiveness of the rapid-prototyping process, to better meet the demanding requirements of digital banks. The length of the cycles is determined by factors unique to each project: project complexity, the stability of its requirements, the frequency of incremental functionality, deployment needs, the number of stakeholders, and the extent of automation and planning maturity. Importantly, the iterations within the cycles are sequenced according to definite criteria to increase efficiency of developers and testers while reducing technical risk. Several criteria can be used for sequencing iterations:

Ёё Logical grouping.Work completed in the iteration is a complete module that can either be released internally or externally.

Ёё Business priority.Ensure functionality that is most critical to business is delivered as early as possible.

Ёё Dependencies. Align iteration to meet all required dependencies with other projects.

Ёё Reusable components. Build components that will be reused in other modules first.

Ёё Use-case completion. Completing specific use cases in iterations will enable organizations to release to end users and get faster feedback.

Release-based testing

In the continuous solutions process, project-focused testing increasingly gives way to release-based testing. In this orientation, all development-deployed resources work on a release-based schedule, and limited resources are assigned or associated with particular projects. Crucially, all test cases are tied to use cases very early in the development process. The early linkage between testing and use helps minimize duplicative testing efforts, eliminates project-management overhead in testing, and promotes more extensive end-to-end testing both upstream and downstream.

Release-based testing demands a new level of resource flexibility. The pooling of resources through “multiskilling” and role-based allocation enables the delivery team to be more responsive to variable incoming user requirements and breaks the traditional silo mentality of skill overspecification.

Agile plus lean

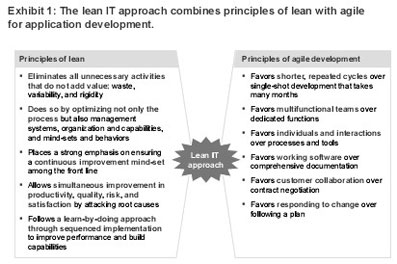

In our experience, a combination of agile and lean principles in application development can help banks build capabilities in continuous solutions development. The approach leverages deep business-IT integration to create solutions that deliver quality, speed, and lower overall cost. The lean focus eliminates non-value-adding activities while emphasizing human interactivity and the technical processes. A shift in mind-sets toward continuous improvement helps enable root-cause analysis and improve productivity, quality, risk, and satisfaction. Lean fosters a learn-by-doing approach to capability improvement, so that talent development becomes integral to product development.

The principles of agile development ensure shorter, repeated development cycles by establishing flexible, multifunctional teams in which individualsand interactions are emphasized over processes and tools. Working software is favored over comprehensive documentation, and an attitude of customer collaboration and responsiveness to change is encouraged as the norm, rather than rigid contract negotiation and adherence to preset plans (Exhibit 1).

3ЃЎ Next-generation infrastructure

Next-generation infrastructure (NGI) has emerged as a holistic transformation option for CIOs of digital banks. Essentially, NGI is a highly automated infrastructure service-delivery platform built with new and open technologies operating at scale. NGI relies on large cloud-provider-level hardware and software to create efficiencies while supporting existing and new business needs. The transformation wrought by NGI would address four key areas:

зїЮЊжаЙњвјаавЕЕФЁАЕкШ§ЬнЖгЁБЃЌ140грМвГЧЪаЩЬвЕвјаавбОзпЙ§СЫНќ20ФъЕФЗЂеЙ

газЈМвдЄбдЃКеЙЭћЮДРДЃЌвјааНЋВЛдйЪЧвЛИіЕиЗНЃЌЖјЪЧвЛжжааЮЊЁЃIBMзїЮЊвЛМвЖд