- ПьНнЫбЫї

- ШЋеОЫбЫї

Ёё Banks do not have to pioneer this process; they can learn from other industries and then incorporate valuable lessons into their own change programs.

Ёё More than 600 processes are executed at a bank, and they can be realigned to deliver a seamless digital and multichannel customer experience, reduce value leakage, and increase efficiency.

Ёё Governance and performance-management tools are also critical components of a digital transformation.

Ёё Rapid-process digitization allows banks to surmount the barriers and complexities of their lagging operating models and meet the challenges of a digital-banking future.

The need for transformed operations in Asian banking is not simply a matter of keeping up with Western peers; rather, it derives from the expectations of a growing number of customers in Asia for a digital-banking experience. The pressures are encouraging Asian banks to move sooner rather than later. However, the digital bank puts heavy demands on banks’ operating models.

Digitization of processes, end to end, is both an essential enabler of banks’ digital customer propositions and a significant driver of value in and of itself. Process digitization is different from pure automation in that it not only creates cost efficiencies but also value, by responding to customer demand for new and better products and services. A new approach that focuses on value is taking shape, based on the following actions:

Ёё Creating a customer-centric experience from the start, by focusing on customer satisfaction with the right products as well as on engaging, best-in-class customer interfaces

Ёё Developing tailored, multichannel capabilities to serve the bank’s existing and aspirational customer base, with a state-of-the-art self-service experience that is seamlessly integrated with higher-touch channels such as video, chat, and face-to-face contact

Ёё Offering a simpler product set rather than trying to provide everything; provide the solutions that people want as transparently and simply as possible

Ёё Simplifying end-to-end processes, by identifying and optimizing the processes with the most potential while ensuring that customer needs are put above all else.

By pursuing these principles in a tailored way, banks can transform their operating models to support their customers’ digital-banking expectations. The value at stake in getting process digitization right is significant. Not only are the opportunities for creating cost efficiencies and scalability great, but better service of the customer base will lift revenue and reduce leakage for the bank. The digital bank of the future will succeed only by meeting the needs of a rising generation of digitally savvy consumers who will set the parameters for the next banking experience.

Toward a high-functioning, customer-centric operating model

Digital-banking customers expect a flawless experience, so banks must begin their journey toward end-to-end process optimization with customer centricity. Much is expected of the new model, which has to accommodate continuous innovation in products and services, multichannel distribution, and digital product fulfillment. It also has to enable closely targeted cross-selling and upselling opportunities as well as manage risk and governance.

Four powerful levers

Leading companies in other industries have successfully developed just such innovative operating models, applying four powerful levers: automation, lean, offshoring and outsourcing, and centralization. The transformations accomplished in the manufacturing sector, which not long ago was regarded as a technological laggard, are exemplary. Jumbo airliners are now assembled in three weeks. Automakers are increasingly using lean approaches to drive down defect rates to historic lows. In many industries, infrastructure and back-office functions such as human resources and finance are now completely outsourced to low-cost locations. The employees of business services such as call centers are increasingly being centralized in strategic hubs.

In banking, these same approaches have begun to take hold as leading banks start on the transformation journey—especially when it comes to standardizing productivity to best-practice levels. Even taking into account the differences between banking and manufacturing, banks can learn a lot from these early innovators as they transform their own future operating models.

To meet rising customer expectations of a complete digital-banking experience, banks will have to bypass incremental improvement approaches. Asian banks in both mature and emerging markets will have to accelerate their digital transformations to serve new tech-savvy customers, whose experience with other digitally enabled industries has led to an expectation that banks will deliver a full suite of services in a state-of-the-art digital format.

Optimizing the model along the four levers

A targeted end-to-end process optimization can achieve significant and lasting savings as part of a systematic transformation of the bank’s operating processes. The approach begins with defining how these processes function today and where they need to go in the future. The improvement levers that can deliver this transformation—automation, lean, offshoring and outsourcing, and centralization—have been evolving year to year, improving with the quickening pace of digital-technology innovation. Banks do not have to pioneer the application of these levers; they simply need to learn from others. They can tap into how the levers have been used in other industries and then incorporate this into in their own change programs. By drawing on these valuable examples, the risks of implementation are minimized. Banks can therefore capture the full value of a concerted change program, and can avoid the tendency to employ only one or two levers.

Enormous opportunity remains for a comprehensive approach

An idea of the total value available for capture through a transformed operating model can be seen in the success banks have had after applying only one or two of the transformative levers. Despite the partial approach, these banking leaders have created measureable value in optimizing operations. But full value in operations will only be attained through a holistic approach that addresses all the levers. The value potential in these improvements is very high in Asia, especially emerging Asia, where banks lag well behind their leading Western counterparts in automating banking processes.

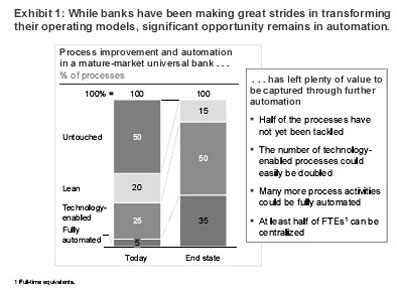

Banks in mature Asian markets have invested more in refining their operating models over the past few years, yet much remains to be done to follow through on the promise of a fully digitized customer experience.

Ёё Only 5 percent of processes are fully automated.

Ёё Only 25 percent of processes are technology enabled.

Ёё Only 20 percent (or less) of the processes have been designed using lean best practices.

Ёё Half of all processes usually remain untouched.

Ёё Most processes are still too complex, requiring unnecessary handoffs across siloed departments and functions, and are clearly not designed for customer and business impact.

The disguised example below demonstrates the great potential for automation that remains even after several optimizing programs have been completed (Exhibit 1).

A cost focus on process improvement

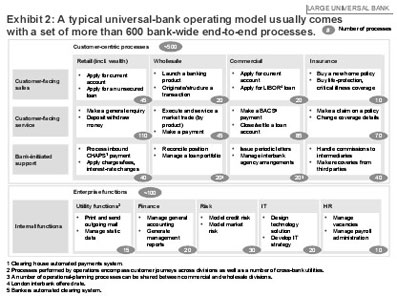

Based on our global work with leading banks, we estimate that all 600-plus processes executed at a bank can be optimized and realigned to deliver a seamless digital and multichannel customer experience, reduce value leakage, and increase efficiency (Exhibit 2).

McKinsey’s experience in the field suggests the potential to automate 75 percent of all processes. This potential extends even to back-office centers that have already undergone multiple waves of lean-transformation, process-enablement technology investments, and even includes the offshoring of selected processes. Most streamlining efforts are made in isolation; the processes that are “leanedout,” automated, and even offshored in piecemeal approaches are themselves tied to a constellation of further processes that depend on manual intervention to a significant degree. This dependence often nullifies the positive effects of the enhancements.

The value potential in process optimization for banks in Asia’s emerging markets is especially high. Most emerging-market banks, benefiting from lower labor costs, have not felt as much pressure to optimize their operating models. However, rising complexity and a shortage of talent are adding to the cost of growing. Many emerging-market banks are therefore beginning to rethink their operating models, with an eye on scalability, efficiency, complexity, and flexibility. These banks are now looking to grow in size but also to enhance their ability to serve their most attractive customer segments. These customers have become much more mobile and technology savvy and are expecting an instant, “anytime, anywhere” experience from their banks.

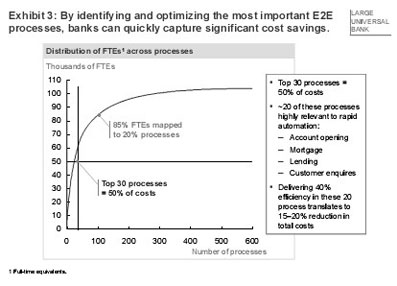

By bringing a cost focus to process optimization, a manageable number of the highest-cost processes can be identified for streamlining. Exhibit 3 shows that 50 percent of costs at a large universal bank were found to be residing in 30 processes; 20 of the processes were highly compatible with rapid automation, including account openings, mortgages, lending, and customer inquiries. By delivering 40 percent efficiency in these important end-to-end processes,a targeted change program reduced total costs by an estimated 15 to 20 percent. At the same time, the program was designed to significantly improve customer service: customer onboarding times were reduced by 99 percent and dramatic improvements were seen in the error rates in customer applications. The bank ran a 12-week, end-to-end process-redesign pilot and rolled out a full program in six months.

Rapid-process digitization

A systematic, holistic approach to a process redesign for the digital future allows Asian banks to create a tailored mix of automation, lean transformation, centralization, or even outsourcing and offshoring, to be applied to each process in a four-part program.

1. Zero-based process redesign. This approach allows banks to reinvent processes based on world-class templates and lean archetypes for bank-process architecture. It can be driven bottom-up or top-down, depending on the organizational appetite for technology transformation.

2. Lean-management best practices. Banks can apply well-established lean-management processes in which management is retrained for performance management and continuous improvement. Areas to focus on include day-to-day flexibility and removing waste and rigidity, but the scope can be narrowed to emphasize core elements such as performance management.

3. Rapid technology development. “Agile scrum” development enables the creation of technology building blocks in an intensive, iterative process. A work-cell team translates concepts into hand-drawn outlines in hours. Within days, these become wireframe mock-ups approved by business; a working prototype is then created and subjected to a daily cycle of review, revision, and feedback.

4. Operating-model build-out. The build-out of the improvements is managed through a dedicated center of excellence. The scope can be adjusted by process and by the extent of the organization redesign; in an accelerated approach, the build-out can be preset within the development cycle.

The approaches to rapid-process digitization can take two forms: balanced and accelerated. The balanced approach is more comprehensive and methodical, requiring more organization-wide buy-in, while the accelerated approach is more focused and intensive, making greater use of disruptive technologies.

зїЮЊжаЙњвјаавЕЕФЁАЕкШ§ЬнЖгЁБЃЌ140грМвГЧЪаЩЬвЕвјаавбОзпЙ§СЫНќ20ФъЕФЗЂеЙ

газЈМвдЄбдЃКеЙЭћЮДРДЃЌвјааНЋВЛдйЪЧвЛИіЕиЗНЃЌЖјЪЧвЛжжааЮЊЁЃIBMзїЮЊвЛМвЖд