- ПьНнЫбЫї

- ШЋеОЫбЫї

Ёё Digital showcase center.A few innovators are transforming branches into centers that showcase their mobile and digital capabilities. While these centers tend to have a nonbanking,tech-driven look and feel, they fulfill the bank’s need for a physical presence to attract customers. At the same time, they serve as a testing ground for those customers who are increasingly reliant on mobile but not completely proficient in its functionality. Particularly prevalent in highly populated areas, such as Hong Kong and Singapore, showcase centers feature multiple screens and devices where customers can test, play, and learn with support from staff. This format, however, is yet to be proven as economically sustainable.

By analyzing its customers, a bank can determine which center format is best suited to the needs of its specific customer segments. A number of banks are employing all three formats in carefully selected micromarkets. The question for Asian banks becomes how many branches they should transform, which types of centers should be used and in what combination, and which specific geographic areas they should target.

Use data strategically

The evolution of the consumer journey from one physical channel to multiple channels has come with challenges. However, the explosion of digital channelspresents an important opportunity—new sources of highly informative, external data on consumers.

Customers who rely on one or two channels exclusively provide a bank with some basic data about themselves, such as a customer profile, account balance, and transaction records. The bank’s understanding of these customers is limited to the structured data it can gather from internal systems. In contrast, customers who use multiple channels—and digital channels in particular—give banks unstructured, external data on their Web behaviors. Banks employing this kind of data must pay scrupulous attention to local privacy laws and customer consent and preferences.

Where available, external data from digital channels can offer banks a significant opportunity. Banks that invest in data and advanced analytics can personalize customer-relationship management across channels. They can use it to build individual product offerings, cross-sell, improve loyalty and reduce churn, identify new customers, structure pricing, inform customer-service models, and manage risk. Additionally, they can use this data to map and identify attractive micromarkets. By zeroing in on the geographic location of specific customer segments, banks can determine whether their footprint makes sense. These insights can help banks rethink branch formats, transform existing branches, and manage resources.

Digital banking is about more than enabling digital channels. Banks that successfully manage multichannel by creating a seamless customer experience, rethinking branch formats, and using data strategically will be able to withstand competition and pressure from new technology players. They will also be better positioned to capture the loyalty of emerging and new customer segments. A subsidiary of an established European bank offers a case in point. By following these measures, the subsidiary acquired more new customers with substantially fewer branches than its parent company over a three-year period.

Chapter 3ЃКDigital sales enablement: How to turbocharge performance and customer satisfaction

(Kirti Avasarala and Ananya Tripathi)

Executive summary:

Ёё The convergence of consumer needs, technology advances, and sales-force familiarity with technology in Asia is opening up new digital-based sales approaches.

Ёё Digital enablement has the potential to significantly boost sales performance and improve customer experience.

Ёё To ensure success, implementation should be business-led, with rapid technology prototyping, and backed by a comprehensive sales-force adoption plan.

Consumer needs, rapid technology evolution, and increasing customer and sales-force familiarity with technology are converging in a way that is making digital sales enablement a tangible opportunity. By digital sales enablement, we mean harnessing the full range of capabilities brought by digital devices and communications and by Internet-based content to support the sales process. Early movers in Asia are already seeing marked improvements in sales-force capabilities and performance, an increase in customer-satisfaction levels, and higher financial performance.

Digital enablement of the sales force and sales process can present challenges, however, and to effectively implement such a transformation, companies must focus on three steps. They must ensure that the program is business-led and thatit is undertaken through an incremental, fast-turnaround prototyping approach that incorporates feedback from the field. They must also back the program with initiatives to transform the mind-sets and behaviors of the sales force.

Why embrace digital sales enablement?

The digital evolution of the Asian financial-services sector is at an inflection point. Consumers are increasingly favoring a digital-technology-based approach when they set about choosing financial products: they conduct online searches, read peer reviews online, and compare product features on aggregator sites. In addition, technology is becoming increasingly accessible to consumers and the sales force with the decline in cost of mobile devices, ever-broadening access to the Internet, and the enhanced ability of software providers to rapidly develop and deploy applications. Finally, many on the sales force are already familiar with technology as part of their private and professional lives. Together, these trends are providing the right environment for a digital transformation of the sales function in the financial-services sector in Asia.

What are the areas that financial-services companies should prioritize? An analysis of the sales funnel in the banking and financial-services sectors points to five areas that can offer the most attractive gains from digital sales enablement.The first is lead generation, addressing two of the time-honored challenges that face sales staff: identifying which customers to meet and coping with shortages of new-customer prospects. Continuing expansion of digital-data availability and of social media is opening up major new areas of opportunity for lead generation.

The second area is provision of new digital-based tools to enable salespeople to provide customers with a higher-quality and differentiated sales experience that includes interactive functionality. Demand for such higher-quality sales approaches is increasingly coming from better-informed customers. They demand a more professional, needs-based sale, rather than the relationship-based sale that financial players have traditionally provided. A digital-based approach that includes interactive functionality can meet this need. Digital-based tools can also help raise the quality of interactions with customers uniformly across the sales force. Our research shows that a large part of the variation between top-quartile and bottom-quartile salespeople (representing a performance variation of between 100 percent and 300 percent) is driven by variability in the quality of the sales process.

The third area is streamlining fulfillment. Financial players face an ongoing need to reduce the time and effort wasted on manual processes associated with the sales process, which can frequently lead to sales leakage. Examples include cases of the same data being collected several times, the time-consuming process of having customers fill out and return paper forms, and the need for repeated meetings with clients.

The last two areas that financial-services companies should prioritize are capability building among the sales force and performance management. With high attrition in sales forces (in many cases above 50 percent per year), technology provides a scalable and sustainable method for capability building. In addition, digital sales enablement helps financial companies to not only better manage the real-time performance of their sales force by creating transparency into what they are doing, but also monitor all the digital sales enablement modules.

Defining a digital sales enablement program

To implement digital sales enablement and to capture the greatest range of benefits, we believe that an approach that comprises six “modules” is required. The first five modules cover the areas that offer the most attractive gains through digital sales enablement; the sixth module links up the new digital sales approaches to the institution’s legacy structures.

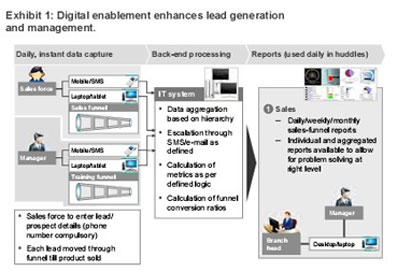

Lead generation and management

Using big-data approaches and tapping into social media (where privacy and all relevant laws permit), financial players can combine rich, internally available data such as customer-transaction histories and profile information and external data to divide their customers into microsegments. They can then provide their sales force with simple, targeted next-product-to-buy leads. Such digital enablement makes it possible for the salesperson each morning to log on to his or her device to find a set of customer leads (allocated to him by geographic mapping) that have been triggered through back-end customer analytics (for example, analyses of transactions at the bank or a life event such as marriage) with a clear recommendation on what should be the most relevant product pitch (Exhibit 1). Our experience shows that there is an up to twofold difference in conversion efficiency between a high-quality lead such as these compared with a cold lead.

Interactive sales tools

Digital technology can help boost sales performance by enforcing a standardized and higher-quality sales process to meet consumers’ more sophisticated needs, and to help to level out variations in the performance of salespeople (Exhibit 2). This module includes user-intuitive sales processes, such as a fact finder and graphical financial-goal-management tool. These can be supported by videos, product comparisons, and interactive fact displays to address frequently asked questions.

A financial-services player in Germany that implemented such a user-intuitive digital sales approach saw substantial improvements: its number of satisfied customers increased by 300 percent, while sales-force productivity increased by 40 percent overall, as the gap between top- and bottom-quartile performers narrowed. Another company saw more than 70 percent of customers awarding a maximum score on a feedback scoring metric for their satisfaction with a new digital sales process and also saw a 25 percent increase in the average value of products sold.

Digital fulfillment

Putting in place a digital process that minimizes manual data entry and the need for paper and is highly automated (to facilitate straight-through processing as much as possible) can help to ensure quick fulfillment. By speeding up the process, it can help to plug the leakages that can occur between sale and closure. Using mobile phones enabled with point-of-sale capabilities, a life-insurance player in Vietnam has made it possible for its agents to sign contracts with customers in 24 hours, a time frame that before the use of this technology was not possible. Similarly, a life insurer in India has invested in making its sales process paperless and guarantees a four-hour turnaround time to the customer for policy issuance.

Performance management

To capture the value of all the modules of digital sales enablement, players should invest in a performance-management system designed to monitor the activities related to the modules and related digitally enabled activities. This system can help players enforce discipline in the sales force, as well as keep track of the inputs and corresponding outputs and therefore tightly monitor the sales funnel. Such a performance-management system can have varying levels of sophistication, based on performance thresholds and deep analytics. These can range from basic sales-funnel reports to triggers and alert escalations (for example, sending a short-message-service alert to supervisors if a salespersonhas delayed meeting a customer). Finance companies have seen improvements in sales performance of as much as 20 or 30 percent within a year following the implementation of this approach.

Capabilities and connectivity

Technology opens up a range of opportunities to carry out sales-force capability building, with the added benefit that the instruments used can be made available on demand. Such opportunities include the creation of relevant games, videos, e-lessons, and testing. When teaching best-practice sales processes, successful companies often award a certificate to employees who do well, which provides additional motivation. Likewise, putting in place a collaboration and connectivity platform across the sales force can also help to build employee motivation and opens up an opportunity for the sales force to share its successes and best practices.

Multichannel integration

As finance companies move to digital enablement of their sales operations, it is essential that they carefully manage the integration between their traditional manual or physical routines and the new digitally enabled ones. For example, the boundaries between the digital and physical world are blurring as customers are increasingly researching online and then purchasing offline. Financial-services players’ sales and service processes must change to accommodate this trend.

One bank that responded to the change in sales landscape is an Indian bank, which created a seamless multichannel account-opening process tailored to customers who like to take advantage of both digital and physical tools and products. In the course of one day, a new customer can interact with the bank across all of its channels—online, mobile, call center, and in-person relationship manager—and open his or her account. The customer logs in basic details to apply for the account online, confirms the transaction through a one-time password provided over his or her mobile phone, receives a call from the call center within five minutes to confirm the product purchase, and the next day, a bank sales person comes to the customer’s office or residence to collect the necessary documents and close the transaction. The bank is seeing a significant uptick in sales since the launch of this process, especially in the metropolitan areas.

Challenges in the way of digital sales enablement

When undertaking a digital sales transformation, players frequently encounter a number of common pitfalls.

Financial-services companies often define the transformation as a technology-led undertaking. By doing this, they tend to set the project on the wrong course, because the program frequently ends up focused on issues that are not aligned with the business’s priorities, and it is not designed with the ability to generate impact. Embarking on a technology-led course also often fails to win the buy-in of the business side of the organization, which is ultimately responsible for driving the transformation.

The technology mind-set can sometimes lead companies to take a “big-bang approach” to digital sales transformation, attempting to achieve transformation across all modules and implement all technology interventions in one stroke. Such initiatives tend to run into delays and budget overruns, which, in turn, extend the time it takes for the organization to see any real impact. In the absence of evidence of any business value being captured, organizations then lose patience with the transformation. Taking a big-bang approach also often sets a timeline that precludes incorporating feedback from the field into the design of the solutions, which leads to problems at the implementation stage.

In addition, many companies do not focus enough on capability building and on encouraging mind-set and behavior shifts in the sales force. Any change in an organization’s way of operating tends to meet resistance in the sales force. It is therefore important for companies to focus on the incentives and mandates supported by the change story in order to motivate the sales force to adopt the new, digital way of selling products. Many companies still fail to do this.

Finally, companies often continue to maintain two “ecosystems”—a manual one alongside a new digital one—that do not talk to each other. This leads to leakages on the ground. Financial companies therefore need to ensure that the physical and digital worlds merge seamlessly and that there are no break points. For example, companies must have a single system in place through which management can view all sales irrespective of whether they are done physically or using a digital device.

Steps to ensure successful implementation

Any digital sales transformation is only as strong as its weakest link. To avoid the pitfalls we have just described, financial-services players should follow three steps that will help them to capture the full value creation made possible by digital sales enablement.

Make it a business-led design

Players should undertake a business-led diagnostic to identify break points in their sales funnel, and then prioritize the issues that need to be solved by technology. Analyzing the entire sales funnel helps to identify opportunities across customer-facing, sales-management, and back-end-operations processes. To ensure proper linkage between design and execution, the design process should be supported by a dedicated business team that owns the end-to-end design as well as the implementation of the digital sales transformation.

Undertake rapid technology prototypes

For technology development to be both rapid and effective in actually solving business issues on the ground, it is imperative to adopt an approach that creates simple prototypes that users find intuitive and test them early in the field so that feedback can be gathered. This approach ensures that the technology-development cycle is relatively short, and that, because the field sales force is involved early in the testing process, the technology is tailored to on-the-ground business realities. This approach also builds greater ownership among field sales personnel and leads to greater adoption.

Develop a comprehensive sales-force adoption plan

Identifying business issues and designing and refining the technology based on field inputs are important steps. But they are only half the battle. Driving adoption of the digital transformation in the field in ways that ensure the changes will be sustainable is a major undertaking. It requires a significant investment of effort in changing mind-sets and behaviors and includes “push” and “pull” measures—pushes from management and incentives to motivate the sales force to pull.

To carry through the changes, companies must define a “Why do we need to change?” story that appeals to the sales-force personnel at an individual level and makes them want to be part of the transformation. Companies should appoint a group of advocates for the change program in the sales force, and should have a plan in place to communicate success stories coming out of the transformation. In addition, there needs to be a clear capability-building plan that is driven down from the supervisory layers.

зїЮЊжаЙњвјаавЕЕФЁАЕкШ§ЬнЖгЁБЃЌ140грМвГЧЪаЩЬвЕвјаавбОзпЙ§СЫНќ20ФъЕФЗЂеЙ

газЈМвдЄбдЃКеЙЭћЮДРДЃЌвјааНЋВЛдйЪЧвЛИіЕиЗНЃЌЖјЪЧвЛжжааЮЊЁЃIBMзїЮЊвЛМвЖд